It is important for strength to persist, and for reflation expectations to continue to turn up. Should our inflation rotation models sense a change in underlying tone, there is a chance we rotate into bonds. It is for this reason that next week is pivotal. Historically, emerging markets have had many 5%+ weekly up moves. As algorithms begin noticing an end to US momentum and a start to emerging market strength, it will likely become a self-fulfilling momentum trade that very few will see coming.

|

0 Comments

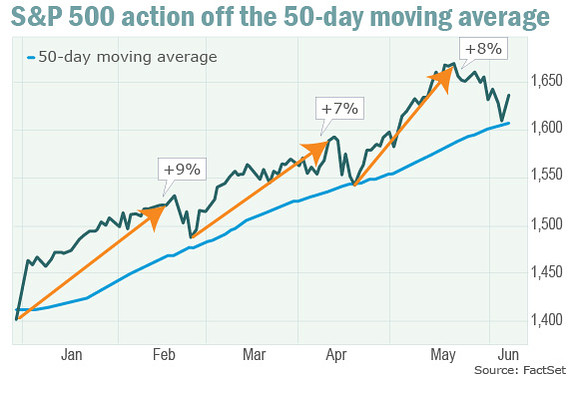

Bullish sentiment is rampant, the CBOE Volatility index (VXX) is bumping along its recent lows, and price/earnings ratios for stocks are entering high, if not nosebleed, altitudes. That makes things ripe for a decent correction after a surprisingly strong summer rally. The revival of the stock market over the last several weeks has been most impressive. After dropping by over -7% from May 22 to June 24, stocks as measured by the S&P 500 Index (SPY) suddenly reversed higher and have spent hardly a moment looking back. In the 18 trading days since the June 24 bottom, stocks have advanced in 15 of these sessions. This is an incredible 83% winning percentage for a market that appeared on the brink of cascading lower when the latest rally got underway. The good news for investors may be that "smart money" tends to sell early while the market is still rising, while there are still bullish investors willing to take the other side of their sell orders. Since making a new all-time high on March 27, the S& 500 has risen 7%. That may make some investors and pundits nervous, but there is little to fear with regard to new highs per se: Stock prices do not mean-revert -- i.e., rather than fluctuating around an average, stock prices tend to drift upwards over time. As the Federal Reserve tightens policy and emerging-market demand cools, we are going to see plenty of unsustainable growth models fail to meet Wall Street expectations and slowly come apart at the seams. Click on the chart below to read the article

In my mind, the Bernanke years at the Fed can be divided up into two parts. After the Alan Greenspan Fed (of which Mr. Bernanke was a part), in an effort to combat the possibility of deflation, kept interest rates so low for so long that it created asset bubbles, the Bernanke Fed, now afraid of inflation created the environment for a financial collapse. This was the first part. As America and other developed nations struggle to recover from the financial crisis, the ongoing challenge now starts to claim casualties in multiple asset classes around the world. Buying into the market now at these valuations could result in a very painful affair, he said. What value investors should be doing is putting together a shopping list for when stocks go on sale.  As if it wasn’t bad enough for the millions of Americans scraping by on paltry interest payments, now they face another threat: the loss of principal on their bonds and other fixed-income assets. The sell-off in fixed income began slowly on May 10, an otherwise uneventful day with no obvious catalyst for any change in sentiment. It picked up steam when Fed sources didn’t step forward to calm markets. Then, in comments to Congress on May 22, Mr. Bernanke said, “We could in the next few meetings take a step down in our pace of purchases.” |

It's always a good idea to keep some good articles, at least I think they are good for reference, so I can go back and read them later.

Archives

July 2014

Categories

All

|

RSS Feed

RSS Feed